In the last decade, the presence of robo-advisors has steadily increased and at Financial Literacy Counsel (FLC), we’ve been seeing more interest from our clients. About 50% of young doctors we work with are incorporating robo-advisors into their investment strategy. So what does this mean for you? Should you consider a robo-advisor?

What is a Robo-Advisor?

Robo-advice is investing on autopilot. These companies utilize software that asks you a few questions about your risk tolerance, financial goals, and investment preferences. The answers are then fed into an algorithm to build your investment portfolio. Robo-advisors are geared towards passive investing and can automate different investment strategies such as Modern Portfolio Theory to construct portfolios [1].

Advantages of a Robo-Advisor:

How Do Robo-Advisors Compare to Financial Planners?

To compare robo-advisors and financial planners would be a false equivalency. Truth-be-told, there are robo-advisor applications made specifically for financial planners. Robo-advice can be a strategy that you use independently, with your financial planner, or not at all.

Advantages of a Financial Planner:

1. Comprehensive Planning

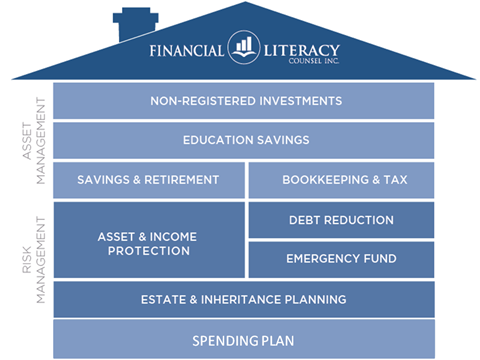

Robo-advisors are just one tool in your financial planner’s toolkit. FLC uses a framework that incorporates the 9 rooms of your financial house when building an integrated financial plan. Robo-advice only covers a portion one room: Investments. An integrated financial plan is the roadmap that will move you towards reaching your life goals.

A financial planner can also work with you and your family to diagnose financial issues and work towards solutions.

2. Expert Knowledge

You may have complex and specific financial needs that can be addressed by a financial planner. FLC has worked with doctors for over 15 years and understands your unique journey. Along with access to financial planning tools and knowledge, which are not available to the public, we also have access to a network of accountants, lawyers and other professionals to meet your financial and incorporated practice needs.

3. Personal Relationship

Financial planners take the time to get to know you and your financial goals on an ongoing basis, which can translate into a more personalized investment portfolio. They are truly on-call and can be consulted on all decisions within your integrated financial plan, while the on-call support from a robo-advisor may be limited in their ability to alter the algorithm-controlled portfolio, or provide legal, tax and investment recommendations.

We know people’s relationship with money can be complex and the value of money is more than just dollars and cents. FLC therefore fosters personal relationships with our clients building trust and motivation to collaborate towards financial well-being.

Because we are not robots; changes in our life can affect our emotions and attitudes towards our investments. Your financial planner can steer you away from a potentially bad financial decision or coach you in the face of uncertainty, something robo-advisors cannot do. Money isn’t just about your account balance—it could mean saving towards a child’s future, a family home, or an emergency fund. Financial planners understand the emotional importance of each financial goal.

While robo-advice is becoming increasingly popular, the choice to utilize it in your financial planning strategy is up to you! Before choosing, be sure to do your research and weigh your options to truly assess the value of time and money saved.

If you have questions about financial planning, you’re welcome to book a consultation with one of our advisors.

This article was written for BC Doctors of Optometry Eye Digest Magazine.

[1] Hayes, A. (2021, October 26). Robo-Advisor vs. Financial Advisor. Investopedia.